FinTech

October 28, 2022

More like this

Learn more

FinTech

April 9, 2026

QR-code payments in Czechia: why they took off and what merchants can learn

Learn why QR-code payments became mainstream in Czechia, how instant bank transfers helped adoption, and what merchants can learn when entering the market.

FinTech

November 6, 2025

Barion Wins “Fintech of the Year 2025” at the Visa Awards

FinTech

November 30, 2022

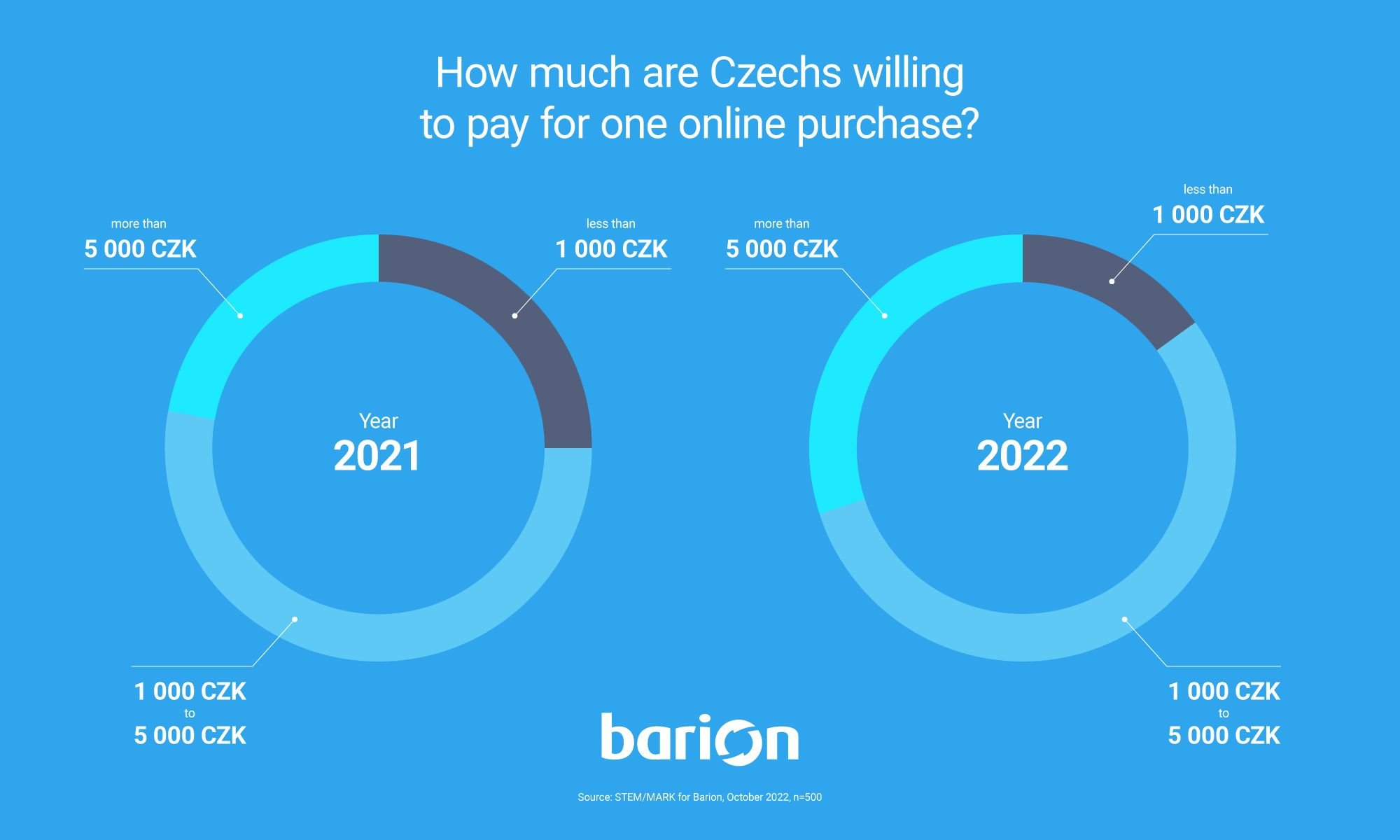

The latest online payment trends in the Czech Republic

Catch up with the latest trends and tendencies of the e-commerce sector and digital payments in the Czech Republic.

Facebook

Facebook Discord dev community

Discord dev community @BarionPayment

@BarionPayment

EU Licensed & Regulated Financial Institution

EU Licensed & Regulated Financial Institution